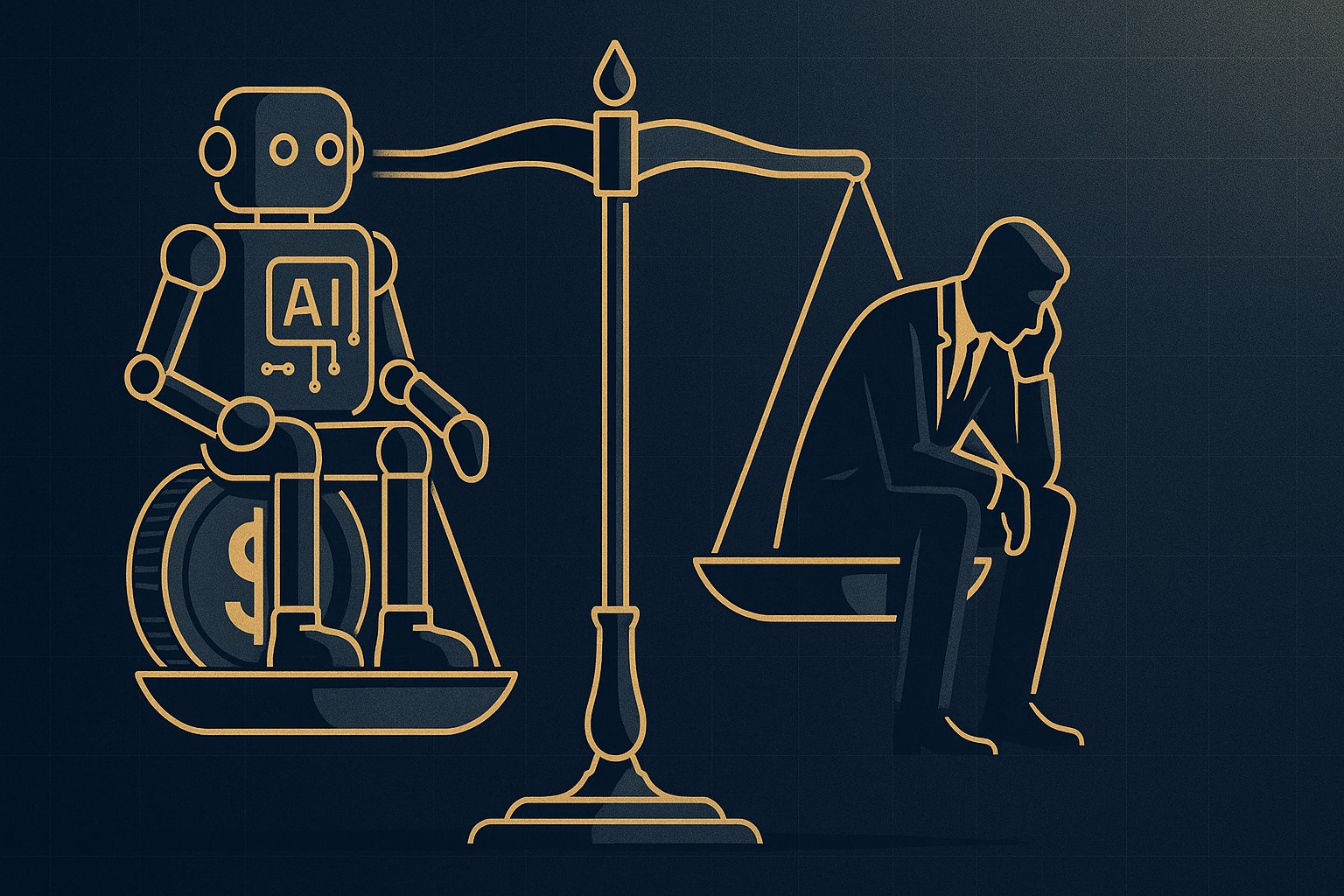

Artificial intelligence, once hailed as the silver bullet for corporate efficiency, is now presenting a harsh financial reality for companies: a choice between investing in AI or in human resources. As AI costs soar, this dilemma is reshaping corporate strategies and exposing a risk that the market has yet to fully acknowledge.

What happened

According to a CNBC report, AI is proving to be far more expensive than anticipated. Companies are finding that their AI budgets, designed to last a year, are being exhausted within a month or two. Arvind Jain, CEO of Glean, and Matan Grinberg, CEO of Factory AI, have both highlighted the unsustainable path of AI spending, with costs doubling with each new model release. This has led to a situation where AI costs are being weighed against human labor costs—a comparison that was historically unnecessary.

Why it matters

The implications of this financial squeeze extend beyond balance sheets and into the broader market. The high costs of AI challenge the assumption that technology will always be cheaper than human labor. This shift could have significant repercussions for corporate governance, as boards and executives are forced to make hard choices about resource allocation. The market, which has been buoyed by AI hype, may not have fully priced in the financial strain that these rising costs impose.

The precedent

This situation echoes past technological revolutions where initial euphoria was followed by a sobering financial reckoning. The dot-com bubble of the late 1990s is a pertinent example, where the promise of the internet led to overinvestment in tech companies that eventually couldn’t justify their valuations. Similarly, the early 2000s saw enterprises investing heavily in enterprise software, only to discover the costs outweighed the immediate benefits.

Postmortem

The core issue is the inefficiency of AI deployment. According to Jain, 95% of enterprise AI usage relies on the most expensive models, even for tasks that could be managed by cheaper alternatives. This misallocation not only inflates costs but also fails to deliver proportional value. Companies are now at a crossroads: continue investing in premium models or optimize their AI usage to better align costs with benefits.

What to watch

Going forward, companies will need to reassess their AI strategies. Key indicators to watch include shifts in AI budget allocations, changes in headcount growth strategies, and the adoption of more cost-effective AI models. The upcoming earnings reports from AI-focused companies will also provide insight into how these dynamics are affecting financial performance.

Moreover, the market’s reaction to these developments will be telling. If investors begin to recognize the financial strain AI costs impose, we could see a revaluation of companies heavily invested in AI.

Conclusion

The dilemma of choosing between tokens and humans raises larger questions about the sustainability of current AI investment strategies. As companies navigate these challenges, they must balance the promise of AI with its financial realities. This could lead to a more cautious approach to AI spending, influencing corporate governance and market dynamics in the years to come.